Proposal to add ENS as a capped collateral to Interest Protocol.

Overview

The ENS token is the governance token to the Ethereum Name Service. ENS holders can engage in protocol governance by delegating their voting power to their address or an address of their choosing.

The proposed parameters and cap are purposely very conservative. After the initial listing, a subsequent proposal could increase the cap.

There are 2 proposals to onboard ENS and AAVE as capped collateral tokens. Upon reading the proposals, I noticed that both are suggesting a 70% LTV. Since the only governance token currently approved is UNI at a 55% LTV, these LTVs seem out of sync with other assets. That said, it is not clear whether the LTVs for ENS and AAVE should be lowered, or whether the LTV for UNI should be raised.

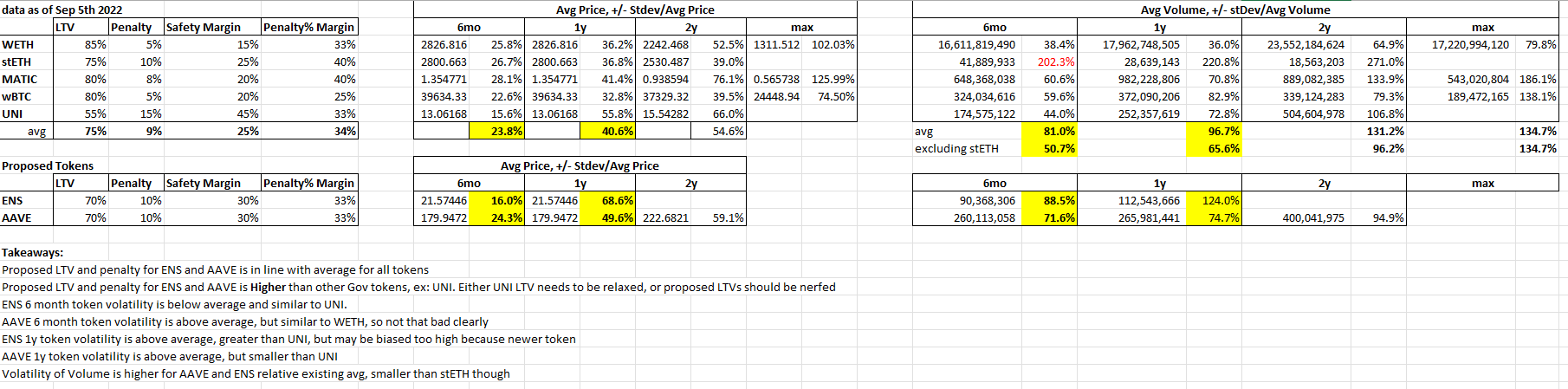

To get to the bottom of this I crunched some numbers using Coingecko’s price and volume figures as of 9/5/2022.

For ENS, we find that:

6-mo price volatility is below average, and very close to UNI’s

1 yr price volatility is above average, although this could be due to it being a new token

Volume volatility (ex outliers) is 60% above average,

For AAVE, we find that:

6-mo price volatility is above average

1 yr price volatility is above average

Volume volatility (ex outliers) is 15% above average

For UNI, we find that:

6-mo price volatility is below average.

1 yr price volatility is above average

6-mo volume volatility (ex outliers) is below average

1 yr volume volatility (ex outliers) is above average

Generally we find that UNI is a less volatile token and that is poses less of a risk to Interest Protocol than both ENS and AAVE. As such, AAVE and ENS tokens should not have higher LTVs than UNI. Either the UNI LTV should be raised, or the proposed ENS/AAVE LTVs should be lowered.

The main difference between this ENS post and @Llama’s Aave proposal is that UNI is uncapped, whereas ENS and Aave are capped. UNI was added to the protocol before Capped Collateral existed. A governance proposal could add capped UNI to the protocol with a higher LTV than the uncapped listing.

That sounds perfectly reasonable. Since UNI holders can vote it in, there is no reason to alter the existing UNI LTV.

As for LTVs on Interest Protocol generally, I think the hierarchy makes sense. WETH has the most-favored LTV at 85%, followed by wBTC and MATIC at 80%, as they each represent native tokens. Then stETH is appropriately set at 75% as it is ETH twice removed. Finally, UNI is set to 55% because it is uncapped. If we take this sample of tokens to be representative of Interest Protocols underwriting standards, it stands to reason that any new collateral proposals should be of the same standard as that of the existing collateral pool. I believe that my analysis has shown that the price and volume volatility of AAVE and ENS are not out of line with Interest Protocol’s other tokens. Specifically, I observe that that 6mo Stdev as a % of avg token price for ENS and AAVE are 16% and 24.3% respectively, whereas the average for the existing pool is 23.8%. Furthermore, when we analyze the 6mo average daily volume, we see that the total caps for ENS and AAVE, $5 million and $20 million respectively, make up just 5.5% and 7.7% of their tokens respective 6 mo average daily trading volume – small potatoes.

To help us make future proposals that are in line with this one, I suggest that generally, Capped Collateral tokens should follow these easy heuristics:

Have a minimum 6 months of price/volume data

Set their Max Cap at no more than 10% of the 6 mo avg volume data at time of vote.

The token’s 6mo stdev/ avg price should be less than 30%. If it is, then an LTV of 70% is appropriate.

When setting supply caps, I put a lot of emphasis on volume and liquidity. It is always better to start more conservative and then increase the exposure in time. Once there are Users depositing and borrowing USDi, we can then look at the distribution of User’s positions and asses what a given % price change would do to the pool. The critical function is to assume there is ample liquidity for liquidators to use when clearing bad debt which could emerge in adverse market conditions.

Great to see you on the forum and contributing. I really want to encourage others to get involved in the community.